If you’re in the market for life insurance, it can be challenging to decide which policy is best for you.

While there are many options for purchasing life insurance, there are two categories of policies:

- Term life insurance — an insurance policy that lasts for a specific time and expires at the end of the term.

- Permanent life insurance — an insurance policy that lasts your entire life and has features that allow you to access your coverage for health emergencies or to build up tax-free savings to be accessed for whatever you like.

Deciding what policy is best for you boils down to where you are in life and where you hope to be in the future. Here’s everything you need to know about permanent life insurance.

What is permanent life insurance?

When you think of life insurance, your mind probably goes to those celebrity endorsement commercials touting the low cost of term life insurance policies. Term life insurance is significantly cheaper than permanent life insurance — term life can be five to 15 times less expensive than permanent life insurance. But if you’re just looking at the premium rates, you’re going to lose out on a ton of potential benefits.

Permanent life insurance is a great investment for younger adults who are facing a wholly different financial future than their parents or grandparents.

“Permanent life insurance is serving that younger demographic who doesn’t get a pension, will not likely receive social security but also are facing a ton of student loans or future medical costs,” says Hanna Wu, Co-Founder and CEO of Amplify Life Insurance. “Younger people have to save more for retirement and medical expenses. By purchasing permanent life insurance at a younger age, you’re able to save for the future.”

An umbrella term for life insurance policies that provide coverage for your entire life, permanent life insurance policies can serve as a vehicle for financial freedom. These policies allow policyholders to save thousands that can be accessed tax-free, invest, and borrow against your policy.

What is the difference between term and permanent life insurance?

Term life insurance provides coverage for a fixed period, while permanent life insurance is for a person’s whole life. But for young people, purchasing a term life policy can leave you losing thousands without receiving any death benefits at all.

“People don’t get insurance until they need it. Then at, say, 35, something happens and they decide to purchase a 20-year policy. At 55, that policy expires and they wind of having to purchase a more expensive permanent policy,” Wu says.

By purchasing a permanent life insurance policy earlier in life when you’re likely healthier, you can lock in a lower premium rate, which will never go up as long as you continue to make payments on the policy. Unlike term life insurance, with permanent life, you can use take money from your policy to cover expenses while you’re still living.

“These are two very different products. With term life, it’s as if you’re renting a house — paying into something without the guarantee you’ll receive any future benefit. But with a permanent policy, it’s like buying a house,” she says.

With that house, you’re getting the opportunity to become financially secure. Wu says people can use their permanent life insurance policy to build an emergency fund (less than 25% of people have emergency savings to cover six months of expenses), for off outstanding debts, or pay for long-term healthcare needs.

How do you access cash from your life insurance?

With permanent life insurance, you’re allowed to use your death benefit to cover medical expenses not covered by health insurance. You can also use it for long-term care needs or for emergencies.

“If you have a stroke and are out of work for a year or more, you can tap into your life insurance to cover your expenses,” Wu says. “Sure when you’re in the hospital, your health insurance can cover hospital expenses. But when you get home, you still need to eat, pay bills, etc. Taking out death benefits in those events allow you to care for yourself in an emergency.”

Unlike your 401K or CD, you do not have to pay taxes on any loans or early withdrawals from your permanent life insurance policy. Additionally, as some permanent life policies have an investment component, you can use those funds as you want.

“About a third of your premium goes to death benefits. The remaining two-thirds can invest in the market or can be put in a high-interest saving account, where you can be generating a 3-4% annual yield or a 7-8% yield depending on your policy,” she says.

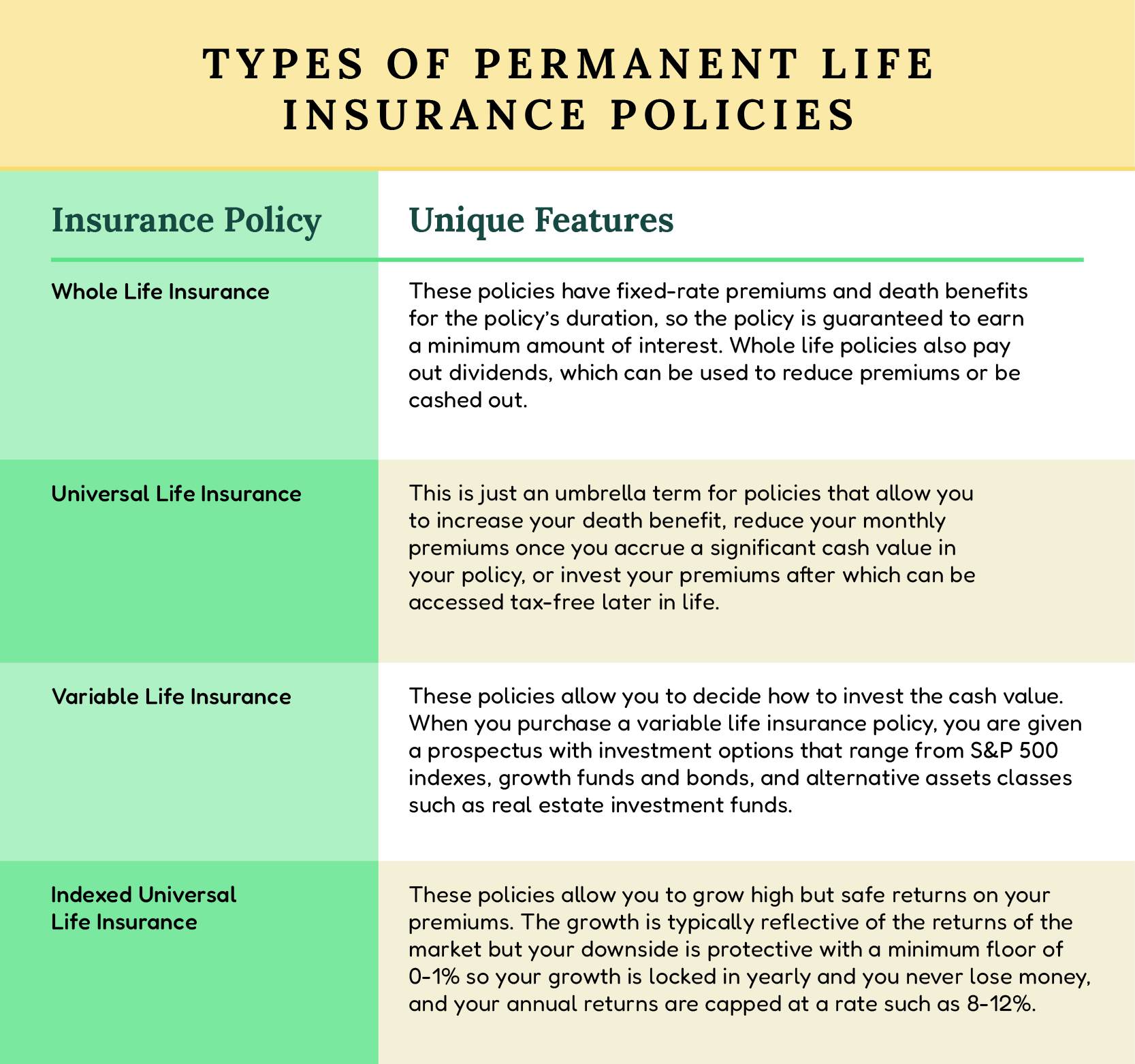

Types of permanent life insurance policies

There are several types of permanent life insurance, each with unique features:

How much does permanent life insurance cost?

Because death benefits are guaranteed, permanent life insurance policies’ premiums tend to be higher than term life insurance policies. The overall cost will vary depending on the type of permanent life insurance policy you purchase, your gender, your health, and how quickly you plan to fund the policy. If you have a shorter payment period, you are likely to have higher premiums.

Is permanent life insurance for you?

- Permanent life insurance isn’t for everyone. But for these policies are beneficial for:

- People who want to lock in a policy that will never expire

- People who are interested in tax-free growth and investments

- People who want to guarantee wealth transfer to their beneficiaries

- Those who want to protect their income in the event of a health emergency (stroke, cancer, severe disability) or for long term care later in life

- Individuals looking to add more to their retirement income and have protection needs

Are permanent life insurance policies worth it?

- There are many benefits to purchasing a permanent life policy, including:

- Lifelong protection

- Cash value growth

- Access to tax-free growth

- Flexibility to choose how to invest your premiums

- Opportunity for money borrowing

- Wealth transfer