So, what is life insurance all about?

Life insurance can feel really daunting, and on top of that, it can feel really unnecessary in your 20s, 30s, and even in your 40s. After all, isn’t it about planning pretty far into the future and managing priorities you aren’t sure you’re going to have? The short answer: No. The long answer: Also no. Here’s everything you need to know about life insurance and why it’s actually a great way to diversify your savings and grow your wealth.

- What is life insurance?

- Life Insurance Myths

- Why is life insurance important?

- What life insurance is right for you?

- Life Insurance Frequently Asked Questions

- TLDR: Life Insurance Facts You Need to Know

What is life insurance, and how does it work?

Essentially, life insurance is a contract between an insurance policyholder and an insurer, where the insurer (or assurer) promises to pay a specific amount of money in exchange for a monthly rate (or premium). In some instances, this payout happens on the death of an insured person. In other cases, the insured person can access funds paid into the policy before the event of their death. So let’s explore the two main types of life insurance a little closer:

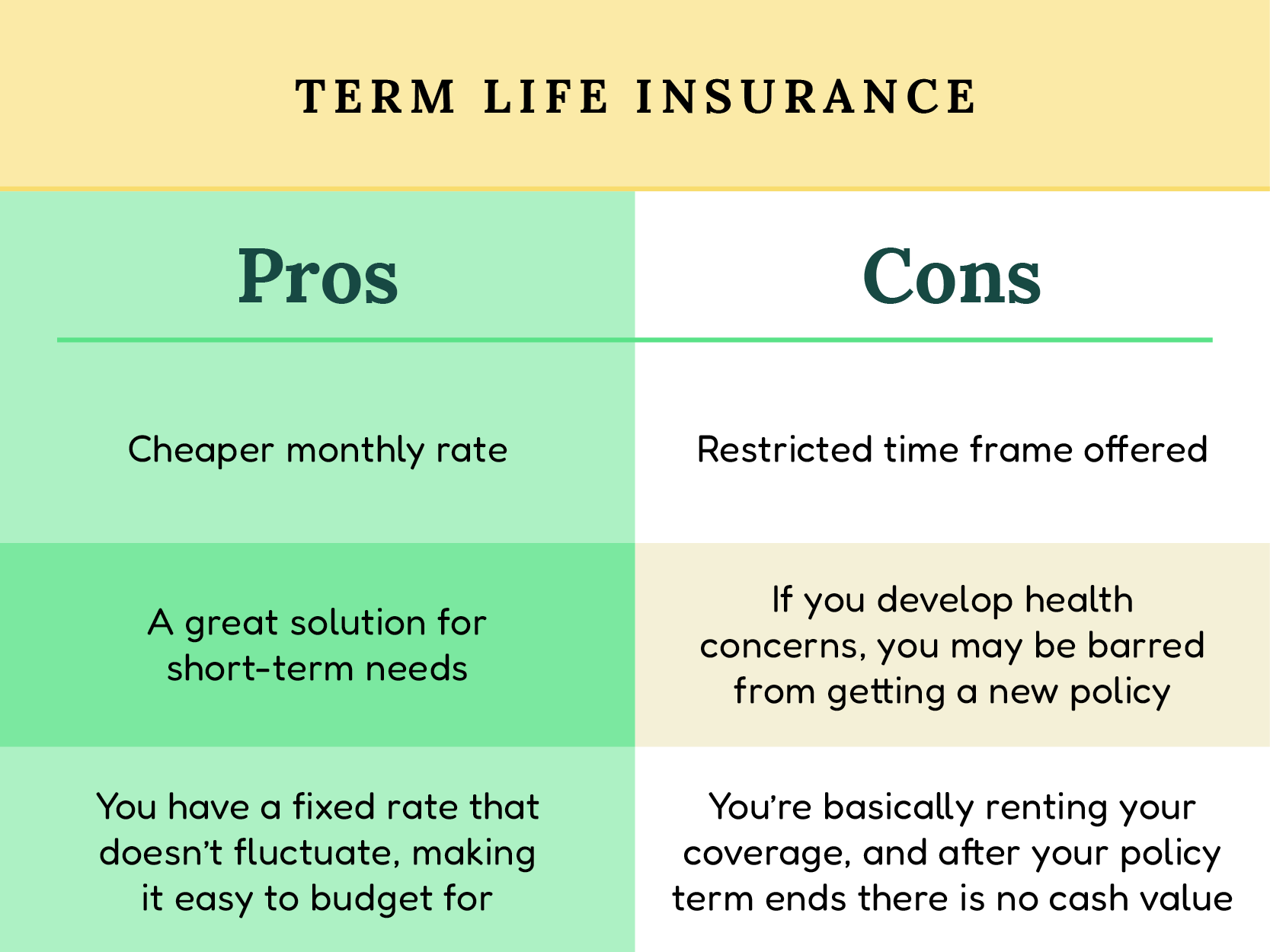

Term Life Insurance Definition

Term life insurance (or term assurance) is an insurance policy that covers the insured for a limited period at a fixed rate. If you’re familiar with life insurance at all, this is probably the kind you’ve heard about. You typically buy a policy for 10, 15, or 20 years, providing temporary coverage for your family or beneficiary in the event of your death (slightly morbid, but true). Term life insurance is typically at a lower premium, especially if you purchase your policy while you’re young.

Here are some of the pros and cons to consider:

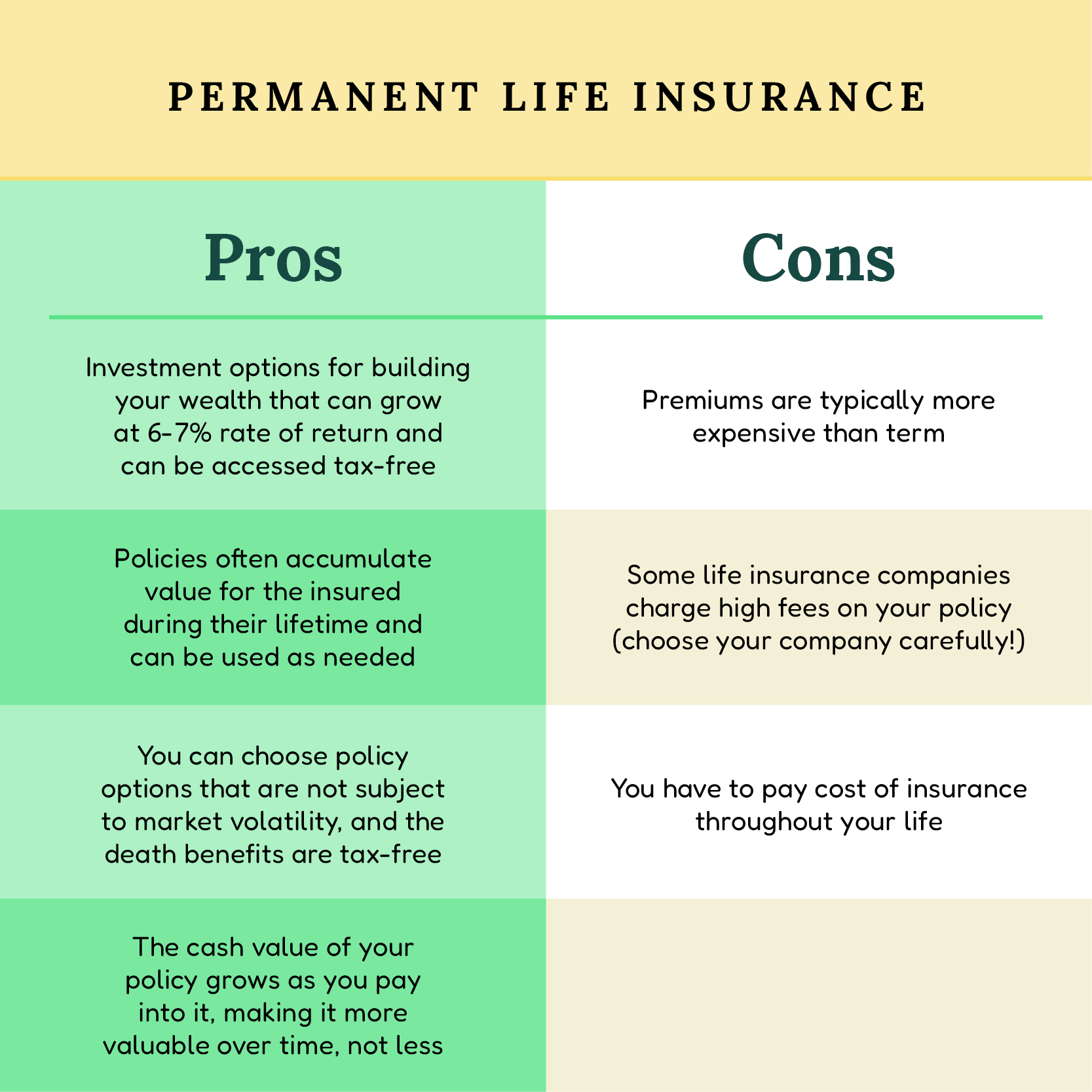

Permanent Life Insurance Definition

Permanent life insurance (sometimes referred to as whole life, straight life, or ordinary life) is a little different. It is not time-based and is a policy that is guaranteed to remain active for the insured’s entire lifetime, as long as premiums are paid. However, there are also other benefits to permanent life insurance, such as building savings for medical expenses or a child's college tuition that you can use while you're alive. (But more about that later.)

Permanent life insurance policies are unique because they can be a great investment tool for younger adults experiencing a different kind of financial future than their parents or grandparents. For example, the Millennial generation is unlikely to receive social security or a pension, but will likely have student loans and future medical costs to contend with. A permanent life insurance policy is a great way to ensure coverage and longevity for your entire life.

Let’s take a look at the pros and cons.

Want a deeper dive into term and permanent policies? Check out our complete guide on the difference between the two policy types here.>>

So what kind of people buy permanent life insurance policies? It’s a lot more common than you think. Here are the stories of a few of our Amplify clients:

A 30-something athlete who wants to build his wealth while he’s still working, with benefits that also give him coverage (and savings) in the event that he’s injured during his career while also helping him save for retirement.

A 40-something 1099 contractor making over 100K a year who doesn’t have a 401K option for herself but wants to grow and diversify her retirement plan with a death benefit, cash value options, and tax efficient market growth.

A 30-something mother of two who is in the process of buying her family home and wants a policy that would help pay off her mortgage and pass on wealth to her kids.

Many of the traditional conversations around life insurance have been term-based, with parents or relatives looking to ease the burden of their passing or protect their family from the expenses associated with getting older. But with permanent life insurance, the conversations are more diverse, including ways to better financial plan—and save—for the future. Want to know more about the fees associated with permanent life insurance policies? Learn about life insurance costs and fees here.

With that being said, let’s go ahead and bust some of the myths that you’ve heard when you asked, “what is life insurance all about?”

Myth 1: You have to pay into a policy for years, and then if nothing happens to you, you don’t get that money.

First things first, this is only true if you have a term life insurance policy that expires. With permanent life insurance, the policy is exactly what it sounds like: permanent insurance for your entire life. This means you build value into your policy as you pay your premiums rather than “rent” your coverage until a certain period. Another good note: When you lock in permanent life insurance in your 30s or 40s, you typically pay a much lower rate, while also growing your wealth with each payment you make. With permanent, you don’t only get money as long as you pay into it, it also never expires.

Myth 2: Only your be

neficiaries can use your life insurance policy. You, as the insured, can’t take money out.

Why’s this one wrong? Because permanent life insurance offers a cash value that you’re allowed to borrow against, or essentially, take out. You have the flexibility to not only use the money throughout your life, but you also can pay more than your minimum to safely grow your policy as savings. Depending on your cash value, you can borrow money out of your policy after the ten-year mark to pay for many

different things: a mortgage payment, your kid's college, medical emergencies, a home renovation, a vacation home down payment, and more.

Learn more about all the ways a permanent life insurance policy is worth it here. >>

Myth 3: Life insurance can’t help you grow your wealth.

This may be our favorite myth to prove wrong. In fact, a permanent life insurance policy is one of the safest ways to grow and protect your wealth as you age. In addition to a 6-8% average return and optional guarantees, life insurance can be a great tool for saving with purpose. Just like you diversify your financial plan with investments, a 401K, and a savings account, you should diversify with a permanent life insurance policy. It is one of the biggest untapped resources for safely building your cash value over time.

Want to learn more about how you can use your insurance policy to make smarter saving choices? Talk with one of our experts today about what your options are >>

Now that we’ve busted a few myths, let’s get to more of the good stuff.

Why is life insurance important?

You already know a little bit about the pros of a permanent life insurance policy, but let’s talk even more about the benefits.

Tax efficient cash growth: Permanent life insurance means you’re paying into a policy that continues to grow over time. And depending on what kind of policy you choose beyond that: universal life, variable life, indexed universal life, or variable universal life, you’re accruing cash value. Because life insurance isn’t technically an investment, there are limits to how much your money can grow, but for those in the know, it is a very good financial benefit to make safe, long-term saving moves while they’re younger. Unlike a savings account, brokerage account, 401K, or IRA, you can access all your growth tax-free.

In fact, permanent life insurance is an excellent cash accumulation and tax diversification strategy designed to give you more money to spend each year. How does that work? For example, you can rethink retirement withdrawals. Instead of taking out 70K from your retirement savings each year, you can reduce that amount by half and take the remaining 35K from your permanent life insurance policy. By doing that, you’ll be taxed at a lower rate for the initial 35K out of your 401K and get tax-free access to the other 35K, saving a lot of money in the long and short term.

Want to learn more about how you can reduce your income tax with your permanent life insurance policy? Learn more about that topic here. >>

Lots of flexibility to use your money

As we already touched on very briefly, the cash value of your permanent life insurance policy can be used starting ten years into your policy, and it’s great for saving for something big, like a child’s education, income replacement, a wedding, or as a way to pay off student loans.

Tax benefits: In permanent life and term life insurance policies, the death benefit is paid tax-free to your beneficiaries. But permanent life insurance is the only type of policy that allows you to grow and access your cash value tax-free as long as the policy remains in effect and the amount you take out doesn’t exceed the cash value. How does that work? Essentially your cash value is a part of your life insurance policy’s “death benefit” that’s grown over time and you’re just loaning against your own death benefit, which you don’t have to pay back (since it’s already yours). It’s also helpful in the event of dividends. If you receive dividends, there are no tax implications.

Want to learn more about the tax implications of a permanent life insurance policy? Check out our full guide on tax-advantaged growth here >>

You can get permanent and term

Permanent has a lot of great benefits, but if you want the protection of term as well, you can do a combination policy that allows you to get both permanent and term coverage. If you are interested in a combination policy, talk to one of our experts today about what your options might look like.

Up next: Figuring out your best move to get a plan that fits your needs, priorities, and future goals.

How we imagine this conversation will go...

You: I don’t know where to start. What life insurance is right for me? Us: We’ve got you.

Life insurance can be confusing, but we believe figuring out what life insurance is right for you doesn’t have to be. That’s why we created this quick list of things to consider as you figure out what might be the right move for you.

Term life insurance might be for you if…

- You have short-term goals when it comes to life insurance

- You don’t want to consider investment options

- You don’t think you’ll need protection beyond the age of 80.

Permanent life insurance might be for you if…

- You are self-employed or run your own business and want to build your cash value

- You want the flexibility to consider tax-free or tax-deferred options for growing your wealth

- You want to be covered throughout your life

- You want to use your life insurance plan for a number of things: retirement, income, tax savings, etc.

- You want to benefit from the policy while you’re alive

Permanent life insurance also offers a wide range of riders that address long-term care, critical illness, term rides, and more. In many instances, these riders can do two things at once: provide a death benefit and provide for the rider’s use. For example, if you have a 500K life insurance policy, you can use that money either for long-term care for an illness, or $500K can be passed to your beneficiaries after your death. Either way, with a permanent policy, you’ve got more options for how you can use your life insurance than ever before.

Want to learn more? You can explore

whether permanent life insurance is right for you here. >>

Still have q’s? Here are some frequently asked questions our financial experts often get from customers and clients.

What can life insurance be used for?

Most life insurance policies help pay for final expenses after death, whether that be funerary costs, medical bills, estate settlements, or other unpaid debts. And depending on your policy type, they can also be used to pay a mortgage, a child’s college expenses, medical bills, home renovation, and more. For a permanent life insurance policy in particular, the insured can build cash value and access tax-free wealth that can be used at a later time—in retirement, in an emergency, or even just because. Talk to one of our experts today to learn more about how a permanent life insurance policy can work for you.

Can life insurance be a business expense?

Many corporations and small businesses alike claim life insurance as a business expense. As life insurance is an employee benefit in conjunction with health insurance, it is common practice to deduct the cost of premiums for along with other medical benefits paid to an employee. For those who are 1099 status, it is often not possible to deduct a life insurance policy that you bought for yourself, but there are other ways to use a life insurance policy for tax optimization. Get your questions answered about deducting these types of expenses by talking to one of our financial advisors today.

Can life insurance be taxed?

In short—no.Your death benefit is not taxable by law, and since your cash value is technically your death benefit that’s growing, you don’t have to report those returns and it won’t be taxed as income or gains. For more information on how you can use your life insurance policy to grow your wealth tax-free, reach out to Amplify today. We’d be happy to help.

Can life insurance be cashed out?

Yes, and it is one of the best ways to create a well-rounded financial plan as you grow your wealth. The best way to do this is to use a permanent life insurance policy to leverage cash value. After ten years with a permanent life insurance policy, you are able to take out your principal and growth of your cash value. We’ve seen people use the savings to make a cash down payment for a house, to remodel, to pay for medical emergencies, as income in the event of job loss, and many other scenarios. If you’d like to learn more about how you can take advantage of the benefits of a permanent life insurance policy, get in touch with us today.

Can I transfer, change, or cancel my life insurance policy?

Good news: You can alter your coverage amount after getting a policy. Often there are some restrictions around how much you can increase and decrease, which you’ll have to work directly with your provider to understand.

And here’s more good news: You can transfer an old insurance policy to a new insurance policy with Amplify as long as there is cash value inside the policy. Even better, you can make this transfer without any liability using a 1035 exchange, and we’re happy to help you get started - talk to a financial expert at Amplify today.

Is getting permanent life insurance during and after COVID-19 a good idea?

Life insurance enrollment spiked high in the aftermath of COVID-19 and continues to have explosive growth well into 2021 because more and more people are using life insurance as an emergency fund that grows cash value. And unlike traditional term life insurance policies, permanent life insurance with a cash value can be used to pay for car accidents, expensive medical bills, or getting out of credit card debt, to name a few. So whether you’re looking for something to rely on if the worst should happen or just like having the security of a safety net, getting started with a permanent life insurance policy is a smart move.

Want to learn more about the top trends in life insurance? Click here. >>

Which life insurance policy should I get?

Life insurance should match your personal goals, what you plan to do in the future, and be flexible enough to help you plan. That being said, it’s very typical that no two insurance policies are alike. However, we often recommend starting with a permanent life insurance policy for most people for three reasons:

It helps you protect yourself and your beneficiaries in perpetuity. Permanent life insurance is like owning a house versus renting a house—it can be more expensive, but it is a better pay-off in the long run, and you know you're protected no matter what happens. A permanent policy allows you to grow your wealth—it isn’t a payment once a month that you’ll never see the benefit of. With permanent, you can save for the future, make smart tax-efficient money moves, and build a safety net that you (as the insured) can use in your lifetime.

With rates that start as low as $50/month, we can help you build a smarter financial future in as little as 5 minutes. Take our quiz to get started.

TLDR: Here’s what you need to know about life insurance.

This was a lot of information to answer the simple question “what is life insurance” so just to round it all out, here are the KEY TAKEAWAYS to walk away with:

KEY TAKEAWAY #1: Not all insurance is created equal.

Permanent life insurance is the best option for people looking for flexibility and long-term protection. If you also want the benefit of term life insurance policies, a combination of the two is possible.

KEY TAKEAWAY #2: You don’t have to die to benefit from life insurance.

Permanent life insurance gives you options for using your savings, whether it’s for medical bills, a new house, tax optimization, or to help your kids pay for their dream school. You can also use it as income after retirement—whether in ten years or fifty.

KEY TAKEAWAY #3: Good life insurance shouldn’t just be a safety net. It should also help you grow your wealth.

Permanent life insurance can do it all—protect yourself in the event of “life things” while also helping you maximize your cash savings with options to guarantee your funds regardless of the market. Whether you’re looking to grow your money tax-free, or want to add an additional layer to your financial plan, a permanent life insurance policy is a reliable, safe way to grow and save for tomorrow.

In conclusion:

You can finally answer “what is life insurance” with clarity. It’s a protection plan for today, tomorrow, and one of the smartest ways to grow your wealth.

Life insurance may be about protecting people after you’re gone, but it doesn’t have to be the ONLY way you use life insurance. With Amplify, you can save smarter, build financial resilience, and protect yourself today—and wherever you’re planning on going in the future.

Ready to get started? Take a 5-minute break from whatever you’re doing to take our quiz and get connected with a financial expert. We can help you get started building for today—and for tomorrow—right now.