Disclosure:

This content is for general informational and educational purposes only and does not constitute financial, tax, legal, or investment advice. Life insurance policies contain fees, expenses, limitations, and exclusions, and policy features vary by carrier and state.

Life insurance is primarily designed to provide a death benefit. While permanent life insurance policies may accumulate cash value, they are not intended to replace traditional investment accounts. Cash value growth is not guaranteed and depends on policy terms, charges, insurer crediting practices, and, where applicable, investment performance.

Accessing cash value through loans or withdrawals will reduce policy values and death benefits and may increase the risk of lapse. Policy loans accrue interest. If a policy lapses or is surrendered with an outstanding loan balance, taxable income may result. Policies classified as modified endowment contracts (MECs) are subject to different tax treatment, including potential taxes and penalties on distributions.

Indexed universal life insurance (IUL) credits interest based on index performance, subject to caps, participation rates, spreads, and insurer crediting methods. While index-linked strategies typically include a minimum crediting rate, policy values can decline due to charges, loan activity, or insufficient premiums.

Ideally, anyone working full-time hours is setting aside money from each paycheck so they can support themselves if they lose their job. But today, many Americans are one missed paycheck away from being unable to pay their bills.

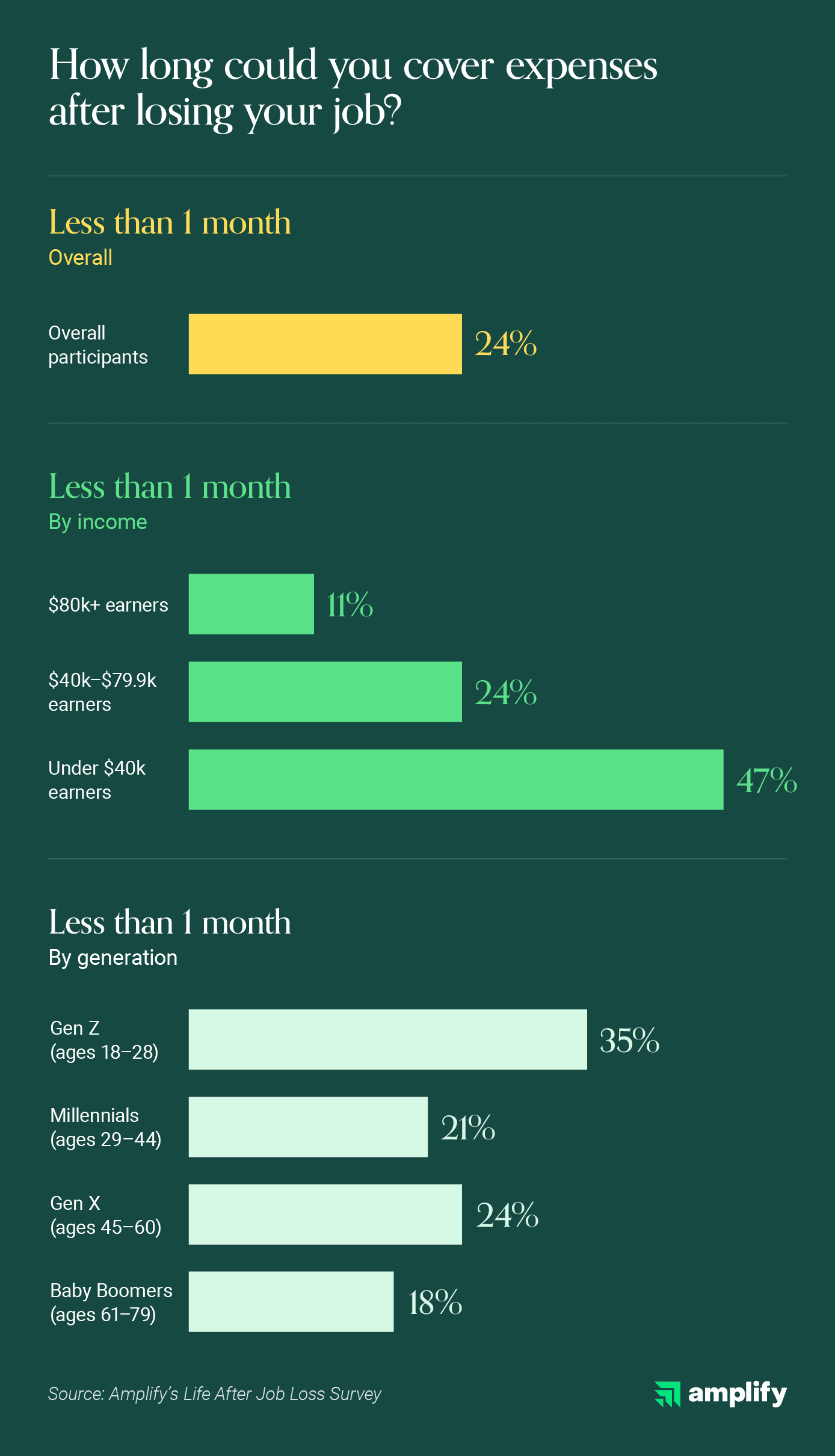

Nearly one-quarter (24%) of employed U.S. adults say they could only cover up to a month of expenses if they lost their primary income today. That figure holds at 24% even among adults earning between $40k and $79.9k — just below the median U.S. household income.

To better understand workers' financial preparedness, we surveyed over 500 employed U.S. adults about how they think about, prepare for, and would respond to sudden job loss. Our results show how workers would pay their bills if they lose their job — and what tools they could be overlooking.

Most working adults are closer to the edge than they think

Nearly one-quarter (24%) of workers say they could only comfortably cover up to one month of basic expenses (like bills, groceries, and everyday spending) if they lost their primary source of income today.

According to the U.S. Census Bureau, the average U.S. household spends $4,484 per month on essential expenses like food, housing, transportation, and healthcare. That means that roughly 1 in 4 workers may not have about $4,000 on hand.

It's not that people aren't working enough. A roughly equal percentage of full-time and part-time workers (24% and 23%, respectively) say they could only comfortably pay up to a month of expenses if they lost their job.

Instead, income plays a much bigger role. The median U.S. household income is $83,730, and if someone makes that much or more, they're more likely to have a savings cushion: 11% of people making $80,000 per year could only pay up to a month of expenses. In comparison, 47% of people making less than $40,000 per year and 24% of people making between $40,000 and $79,999 say the same.

Today, recent college graduates are struggling more than other generations to find work. With that in mind, 35% of Gen Zers (ages 18-28) say they couldn't last a month without a paycheck, suggesting early-career workers are the most financially exposed to job loss.

On the other hand, Baby Boomers (ages 61-79) have had more time to build savings, and they're the least likely generation to say they couldn't survive a month without a paycheck.

- Gen Z (ages 18-28): 35%

- Millennials (ages 29-44): 21%

- Gen X (ages 45-60): 24%

- Baby Boomers (ages 61-79): 18%

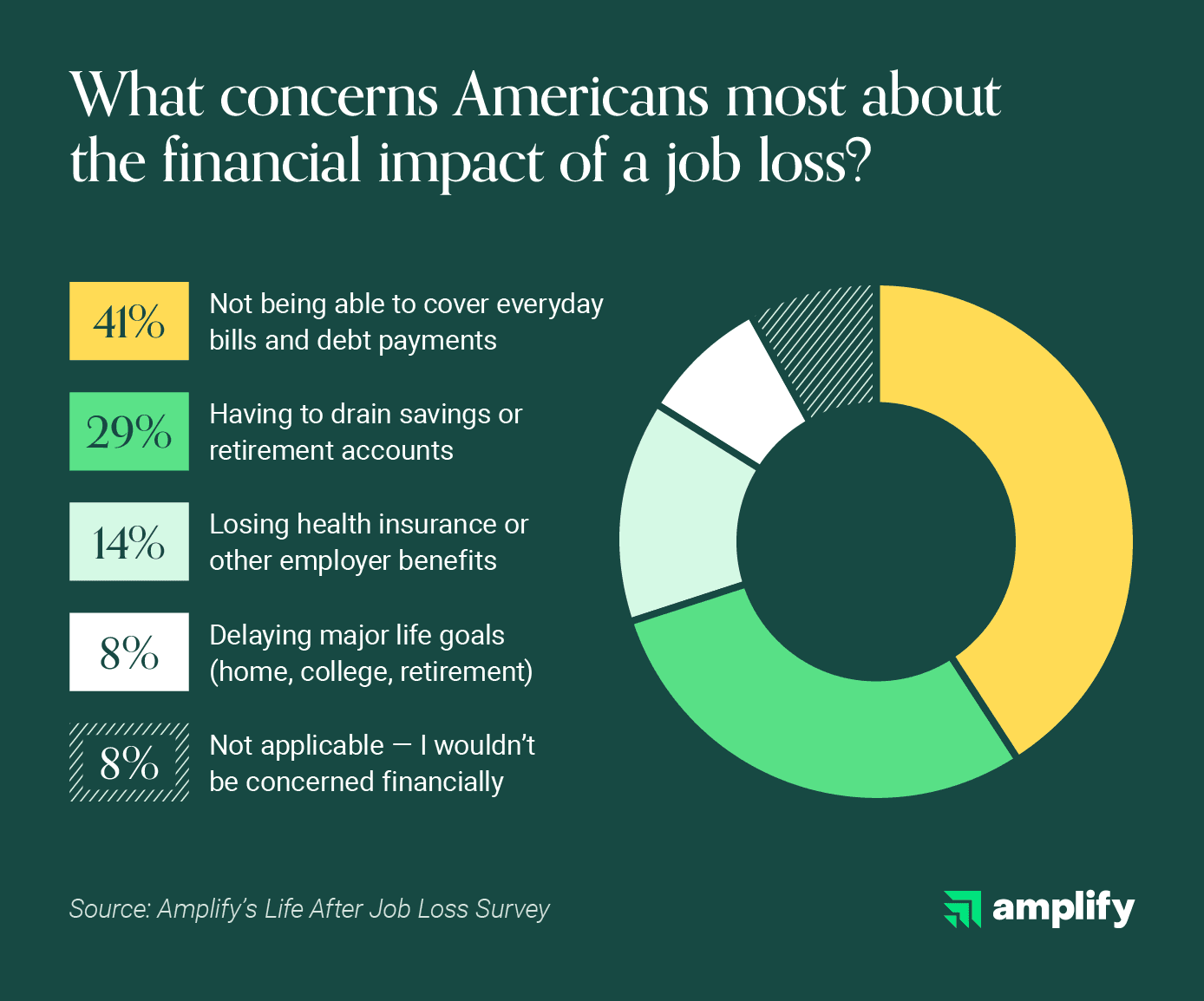

Bills and debt top the list of fears following a job loss

Around 2 in 5 (41%) of workers' top financial concern from theoretical job loss is not being able to cover everyday bills and debt payments.

Savings are the easiest way to pay for immediate expenses in an emergency, but they can take years to accumulate and only weeks to spend. Once savings are gone, they're gone. If that happens, workers don't always have a Plan B.

Workers are also commonly concerned about more long-term financial setbacks, like draining their savings or retirement accounts (29%).

On the other hand, only 14% say their top financial concern is losing their health insurance, suggesting many people expect they could go without or find alternative coverage through options like COBRA or a partner's employer plan.

Nearly half (44%) of workers earning between $40,000 and $79,999 say their top concern is covering everyday bills and debt. They're also the most likely of any income bracket to say a job loss would delay major life goals like buying a home, funding college, or retiring on time.

Middle-income workers are in a tough position: On the one hand, they make enough money that they can consider long-term financial goals. On the other hand, they're more vulnerable than higher-income workers to needing to delay those goals in an emergency.

It makes sense that more people say their top concern is short-term goals. Think of Maslow's Hierarchy of Needs — you need to meet your basic needs before you worry about long-term goals. In today's challenging economy, where the cost of goods have risen in price 25% since the beginning of 2020, many working adults may be in survival mode.

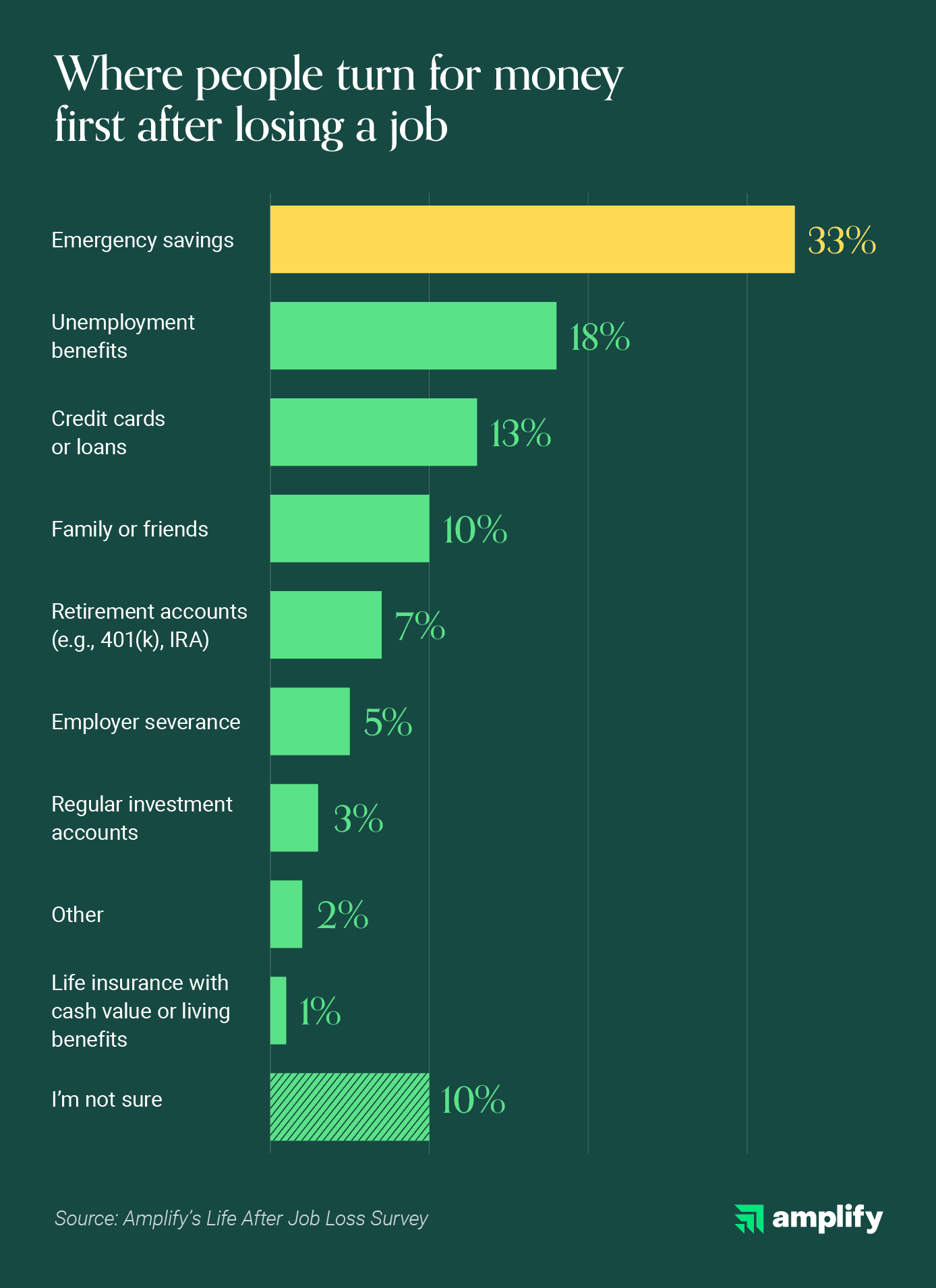

Where people turn first when income stops

An emergency savings fund is a key financial cushion so you can pay your expenses after a job loss, but only 33% of workers say they'd rely on their emergency savings or other cash in the bank if they lost their job.

Instead of savings, the majority of workers would use less reliable or more costly options, such as:

- Unemployment benefits (18%)

- Credit cards or loans (13%)

- Family or friends (10%)

- Retirement accounts (7%)

Relatively few working adults say they would touch their regular investment accounts (3%) and retirement accounts (7%) first. Early withdrawals from a 401(k) or traditional IRA typically trigger income taxes and a 10% penalty, making it a costly last resort.

Raiding a retirement account is a one-way door. If you withdraw from your retirement account, those funds and the compounding growth they would have generated can't easily be replaced. Many people would sooner take on debt or ask family and friends for help before liquidating long-term holdings.

This protectiveness around investments also underscores how dire the situation may be for many workers. If 67% aren't turning to emergency savings first, it may be because they don't have much to draw on.

Around 1 in 5 (21%) of workers making between $40,000 and $79.999 say they would use unemployment benefits first if they lost their job. It's the second-most popular option other than emergency savings, and more middle-income workers would turn to unemployment benefits than other income groups.

Only 1% of workers say they'd tap a life insurance policy with cash value first. These policies include tax-deferred savings on top of an insurance policy, making them a good option for people who need an additional savings cushion, but not enough people may know they're an option.

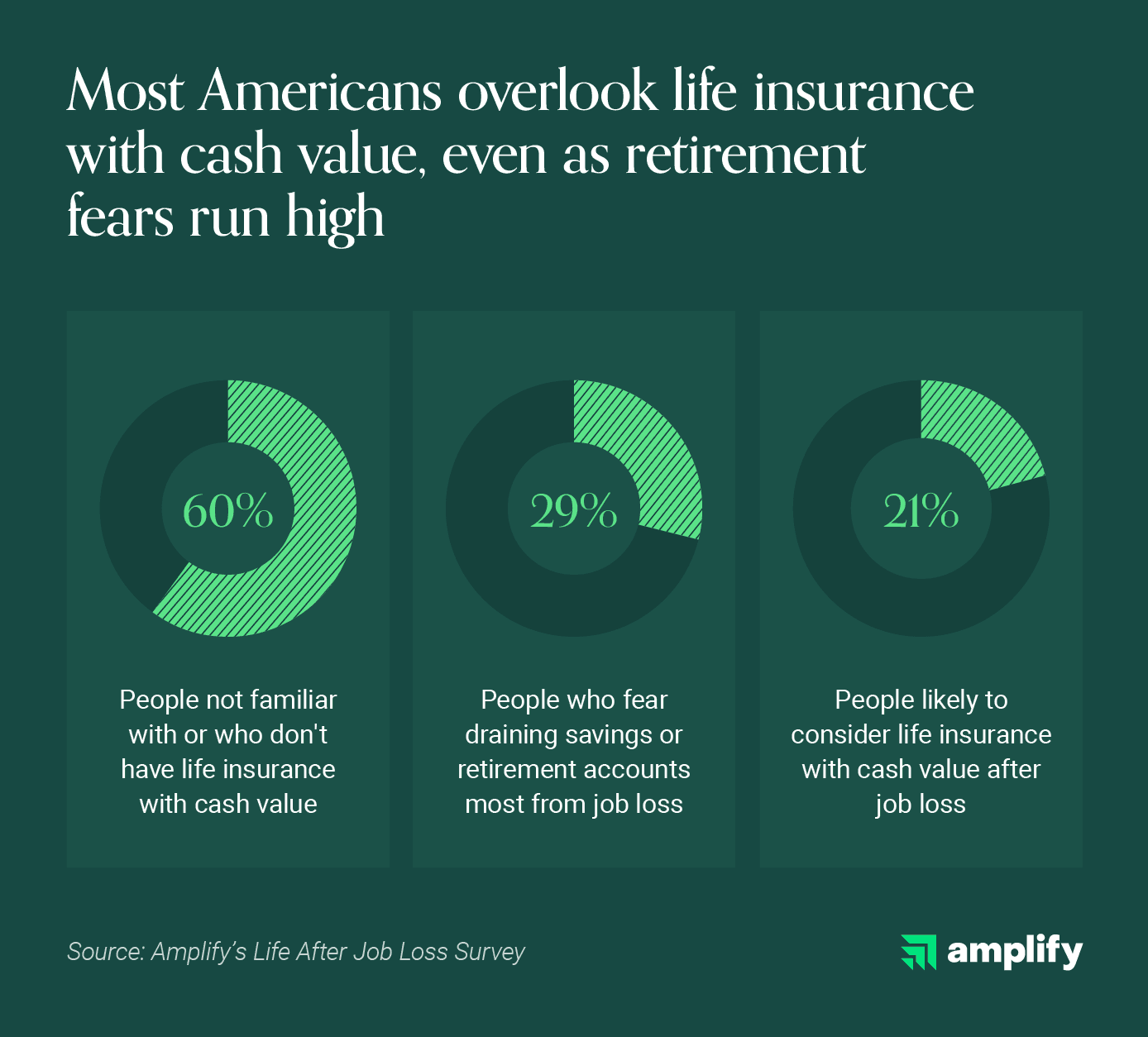

The financial tool most people haven't considered

More than half (60%) of workers say they're either not familiar with or don't currently have a life insurance policy with a cash value. These policies are permanent life insurance that builds a cash reserve over time, which the policyholder may be able to access while still alive. One example is an Indexed Universal Life (IUL) policy, which links cash value growth to a market index, subject to caps, policy charges, and terms.

Just 21% say they'd be likely to consider using a life insurance policy with cash value as part of their financial strategy after job loss, even though it's specifically designed for these emergencies.

This is especially striking given that nearly 3 in 10 (29%) already fear draining their retirement savings after a job loss. Unlike early 401(k) withdrawals, accessing cash value through a policy loan may not carry the same tax consequences. However, loans do accrue interest and reduce the death benefit if not repaid.

Many people likely don't know these policies are an option, which is why adoption is relatively low. Around 1 in 5 (21%) of workers say they're not familiar with using life insurance with cash value as part of a financial strategy at all. For workers who struggle to build a large emergency fund, a well-managed cash value policy could be a more accessible financial resource, though.

Many workers will select a basic life insurance term or group policy through their employer's benefits policy, especially if they're younger or don't have dependents. Without a reason to look further, the possibility of a policy that could also serve as a financial safety net rarely enters the picture.

What life after job loss could look like with a plan

Most working Americans are closer to financial instability than they realize. Without cash on hand, it may be very difficult for them to afford everyday bills in case of a job loss or other emergency. IULs could help build a safety net that isn't tied to an employer, subject to 401(k) withdrawal rules, or dependent on government programs — though it isn’t the right fit for everyone.

Policies must be set up correctly to work as intended, and earned interest may be subject to caps, terms, and policy charges. It works best for those who can commit to consistent premiums over time.

Above all, life insurance is designed to both protect your family and help preserve the financial goals you've worked to build. Ready to see if a policy could play a role in your financial plan? Reach out to Amplify to find out what secure wealth could look like for your family.

Methodology

The survey was conducted by YouGov for Amplify. The survey was fielded between March 5, 2026, and March 6, 2026. The results are based on 1,206 completed surveys, with a focus on the 525 who identified as employed full-time or part-time.

In order to qualify, respondents were screened to be residents of the United States and over 18 years of age. Data is weighted, and the margin of error is approximately +/-3% for the overall sample with a 95% confidence level.